Vulnerability Policy

1. Introduction

The aim of this policy is to enable PJG Recovery Limited’s staff and associates to assess customers that may be regarded by the Financial Conduct Authority (FCA), the Information Commissioner (ICO), the Insolvency Practitioner’s Association (IPA), The Insolvency Service, the Financial Ombudsman Service (FOS) or other regulatory bodies as vulnerable or ‘particularly vulnerable’ in context of CONC 8. This reflects the FCA’s final vulnerability guidance published on 23 February 2021, which is relevant to the provision of debt advice and someone looking to access the Debt Respite Scheme. The IPA is aligned to the FCA definition of vulnerability.

In line with IPA’s expectations, our IP and staff have an awareness and understanding of the issues surrounding vulnerability through regular training. We recognise that failure to correctly manage interactions with a vulnerable person can result in reputational damage and complaints. We do not set any expectation that our IP or staff as medical professionals when dealing with customers, though there is an awareness of some of the indicators that may cause someone to be regarded as vulnerable and treated in accordance with this policy.

Our vulnerability policy has been continuously developed to help ensure all our customers and prospective customers are treated fairly, regardless of their circumstances. It relates to prospective customers and existing customers that are resident in England, Wales and Northern Ireland.

Definition:

A vulnerable customer is someone who, due to their personal circumstances, is especially susceptible to harm, particularly when a firm is not acting with appropriate levels of care.

We want vulnerable consumers to experience outcomes as good as those for other consumers and receive consistently fair treatment from PJG Recovery Limited (henceforth – ‘we’, ‘us’). We have adequate and proportionate systems & controls in place to ensure we manage the risk of harm to vulnerable customers. As part of this risk mitigation, we do not operate debt management plans (DMPs), though we may consider operating Statutory Debt Repayment Plans (SDRPs) when available and The Insolvency Service is available as a money distributor. We can offer a full range of debt advice for residents in England & Wales in association with sister company Clifford Watts Limited, which holds FCA permissions for debt advice and debt adjusting. Clifford Watts has registered to act as a standard breathing space intermediary as an FCA regulated firm with debt advice permissions and staff have completed the Wiser Adviser breathing space training for debt advisers.

We believe that we can demonstrate; how our business model, the actions we have taken and our culture ensure the fair treatment of all customers, including vulnerable customers. We think about vulnerability as a spectrum of risk. This policy has been updated following the publication of the FCA Financial Lives survey in February 2021.

We have considered IP regulatory requirements and looked beyond to the FCA Principles and 6 TCF outcomes in respect of our treatment of vulnerable consumers. We have a TCF policy. We have established an effective policy for the treatment of vulnerable customers and, in some scenarios, to take particular care when serving vulnerable customers. We have implemented clear and effective procedures to identify particularly vulnerable customers (e.g. Customers with mental health and mental capacity issues may fall into this category) and to deal with such customers appropriately in accordance with this policy.

We recognise some customers seeking advice on their debts under credit agreements or consumer hire agreements may be regarded as vulnerable to some degree by virtue of their financial circumstances or low financial resilience. Of these customers some may be particularly vulnerable because they are less able to deal with lenders or debt collectors pursuing them for debts owed. The policy has been adapted in advance of the mental health crisis assessment for a moratorium from 4 May 2021 (Debt Respite Scheme).

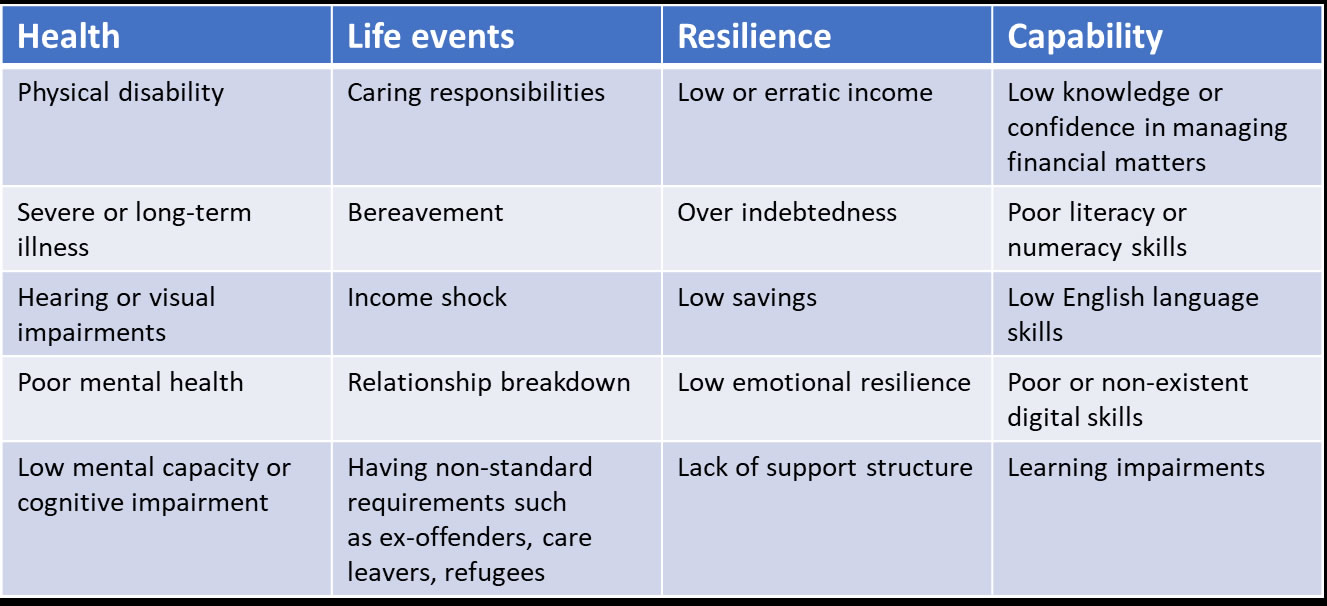

2. Key Drivers of Vulnerability

All customers are at risk of becoming vulnerable and this risk is increased by characteristics of vulnerability related to 4 key drivers:

1.

2.

3.

4.

COVID-19 has added a fifth driver since April 2020.

Not all customers with characteristics of vulnerability will be vulnerable, but they may be more likely to have additional or different needs which, if we do not meet them, could limit their ability to make decisions or to represent their own interests. We try to understand that characteristics of vulnerability are likely to be complex and overlapping, which may influence the spectrum of risk.

The latest version of the policy is intended to follow the FCA final guidance (23/2/2021) around dealing with individuals in vulnerable circumstances and is based around the 6 key FCA expectations in relation to dealing with individuals showing characteristics of vulnerability. These are:

1. Understanding their individual needs and any harms that they may be susceptible to

2. Developing adviser skills, competence and capability to recognise, respond and support an individual or couple showing characteristics of vulnerability (e.g. low financial resilience)

3. Ensuring our products and services are designed to meet customer needs and avoid harm throughout their relationship with us

4. Deliver customer service that helps customers to disclose their needs and which responds flexibly to these needs and communication preferences

5. Communicating in an understandable way with customers and taking into account their communication preferences where the majority of advice is delivered face-to-face or interactively (e.g. by Teams/Zoom) supported by communications in durable medium (e.g. Email)

6. Evaluating, monitoring and taking positive action where vulnerable customer needs aren’t met or where outcomes for vulnerable consumers are not as good as those of other customers. We produce and regularly review MI proportionate to the size and business model of our firm.

We have embedded a consistent approach to vulnerability across our voice, digital and written channels of communication. Given the small size of the firm, we have identified the most common harms that our customers may be vulnerable to. We aim to create an environment where customers feel confident about disclosing their needs. As a small firm this is highly achievable, supported by robust record keeping and a ‘fair by design’ data protection policy.

This policy also takes account of the imminent introduction of the Debt Respite Scheme (4/5/2021) and the requirement to inform the prospective customer of the pros and cons of applying for a standard breathing space.

Before starting a standard breathing space, we consider whether:

▪ our prospective customer has funds or income available to them to pay debts as they fall due

▪ our customer would benefit from entering a debt solution, either now or in the immediate future

▪ a standard breathing space is necessary for us to assess which debt solution is most appropriate, to advise our prospective customer on an appropriate debt solution (e.g. an IVA) or to put a debt solution in place

Before we starting a standard breathing space, we will have given advice to our customer about whether or not a standard breathing space is suitable for them in durable medium. We may involve Clifford Watts Limited in this process where it involves regulated debt advice. Simple eligibility checking can be completed without the need for a referral and can include a vulnerability assessment by the IP or a member of the team that have had vulnerability awareness training.

We can deal with standard breathing space cases, but we would signpost someone eligible for a mental health crisis moratorium to a suitable specialist agency1, in line with The Insolvency Service guidance for Money Advisers (updated 5/3/2021). This is part of our wider commitment to make consumers aware of support available to them, including relevant options for third party representation and specialist support services.

We do not actively target vulnerable customer groups, however, they may become apparent in the initial customer assessment or subsequently by a debt adviser. Due care is required with vulnerable customers at all times. If only one party to the service meets the vulnerable customer policy then discretion can be applied. Customers are to be marked as vulnerable on the internal recording keeping system aligned to the VRS sub-flag categories. This also distinguishes between vulnerable and particularly vulnerable.

Customers in an IVA may become vulnerable at any point in time and this is considered during reviews and any identifiable changes in circumstance. We encourage disclosure by our customers.

The application of the policy at an operational level should always seek to avoid any consumer detriment. We will take reasonable steps to ensure that the customer is able to understand any contract (e.g. IVA proposal) that they are being asked to agree to and their obligations through any such agreement.

Evidence gathering is aligned with some of the assessments in the new Debt Respite Scheme. We routinely access credit reports and review bank statements and other key financial documentation. This may identify unusual spending patterns.

Care will be exercised where the customer has special communication needs (e.g. blind/poor sight, deaf/hard of hearing, speech impediment, physically disabled with limited mobility or mobility restrictions). Some of these conditions may preclude them from using our services.

1 https://england.shelter.org.uk/professional_resources/debt_advice

Encouraging disclosure

IP and staff questions are designed to encourage disclosure and to identify characteristics of vulnerability, for example:

▪ Lack of self-confidence (i.e. there is a risk that any debt solution may be regarded as a distressed purchase)

▪ Low literacy, numeracy and/or financial capability (e.g. may not understand the extent of their financial problems and the implications of these, they may not understand the debt remedies available, including the difference between informal and formal debt solutions)

▪ Low/insecure income, perhaps with a reliance on benefits or non-dependent support

▪ Being unemployed (e.g. determining the period of unemployment, frequency of job loss)

▪ Being responsible for high levels of care for another person (e.g. close family member)

▪ Having a physical impairment (as set out above and may include common problems like debilitating treatment for cancer)

▪ Having mental health problems

▪ Living in social rented housing

▪ Living in a lone parent household with minimal financial support

Where a case is determined (in the judgement of the IP or trained member of staff) to meet the criteria of our vulnerable customer policy then this will be clearly marked on the customer record with a short explanation to support this assessment, mindful that this may be treated as

3. Debt Respite Scheme

We can deal with standard breathing space cases, but we would signpost someone eligible for a mental health crisis moratorium to a suitable specialist agency2, in line with The Insolvency Service guidance for Money Advisers (updated 5/3/2021). This is part of our wider commitment to make consumers aware of support available to them, including relevant options for third party representation and specialist support services.

We are aware of our requirements under the Equality Act 2010.

2 https://england.shelter.org.uk/professional_resources/debt_advice

4. Data Protection Act 2018

We have found the Money Advice Trust and Money Advice Liaison Group’s ‘Practical guidance on vulnerability, GDPR and disclosure’ a useful reference document. We have also benefited from working with our trade association, DEMSA, and professional body, the IPA. The ICO has provided advice and support to trade associations in understanding codes of conduct, meeting the necessary criteria and on complex areas of data protection. We have a separate

5. Mental Capacity Act 2005

This act sets out the legal framework concerning mental capacity. Mental capacity is a person’s ability to make a decision. It is reasonable to assume a customer has mental capacity at the time the decision is made unless the firm knows or should reasonably expect that the customer lacks capacity. Having limited mental capacity does not necessarily mean that the customer lacks capacity to make a decision. The most common cause of mental capacity limitations are: a mental health condition; dementia; a learning difficulty or development disorder; a neurological disability; a brain injury; alcohol or drug abuse. Mental capacity checks have been implemented using FCA Practitioners’ Pack and the MAT vulnerability guide for debt advisers.

Our policy around mental capacity limitations

It is our policy to ensure that we treat customers who have mental capacity limitations with respect and consideration. In our dealings with such customers, we will endeavour to adhere to the following practices:

▪ Not to discriminate against the individual

▪ Not to inappropriately deny a service, though the service does involve some financial capability checks

▪ Assist the customer to make an informed decision

▪ Explain how special category personal data (under DPA 2018) will be used in their case and mark the customer as vulnerable or particularly vulnerable on the core systems accessed by customer facing associates

▪ Where providing debt advice, ensure the debt solution is appropriate and is based on a reasonable assessment of affordability and in the best interests of the customer

▪ Ensure communications are clear and jargon free, providing documentation in a range of medium, but pre-dominantly in electronic format

▪ Make a reasonable assessment of the customer’s ability to understand and retain any information delivered by the debt adviser

▪ Allow the customer sufficient time to make a decision

We have established and implemented clear procedures to support this policy to identify particularly vulnerable customers and to deal with such customers appropriately, whether this involves a referral to a specialist not-for-profit provider or suitably supporting the customer internally. The record keeping systems have the functionality to distinguish both vulnerable and particularly vulnerable customers. Recorded Teams/Zoom calls are now maintained to demonstrate that a meaningful discussion has occurred with the customer or their carer (with authority) with regard to how sensitive or special category personal data (as defined in the prevailing data protection law) will be used.

Our privacy and data protection statements take account of DPA 2018 requirements and were developed after 25 May 2018 and reflect Brexit from January 2021.

We recognise that that an individual’s circumstances can change and anybody can become vulnerable at any time (e.g. through sudden job loss, family bereavement, serious illness). The impact of COVID-19 is a good example of this.

Where mental health or mental capacity limitation (mental incapacity) is a factor then we follow the

6. Identification of a vulnerable customer

The identification of a consumer or customer who could be vulnerable is ultimately matter of personal judgement. This is not designed to be an automated process. When making a judgement about whether a customer is vulnerable, it is important to communicate with the person and make a judgement based on their individual circumstances, rather than making assumptions.

Vulnerability is also not a static state associated with a particular circumstance or situation, it can only be determined by a measured assessment, including whether they are:

▪ upset or distressed

▪ do not readily understand what is being said

▪ are not giving meaningful responses to questions posed

▪ are disproportionately annoyed or frustrated

▪ threaten suicide

Some people will have obvious physical disabilities (e.g. deaf, blind) that may mean they need extra personal support or that adjustments need to be made to enable them to access services we offer. In some circumstances, it may be impractical to access the service. Other people may have conditions that are less obvious (e.g. dyslexia). Judgements must be based on behavioural evidence and structured questioning that may make it necessary to ask specific questions and this may determine suitability to use the service.

The following personal factors may be associated with vulnerability and may require evidence to support products and services we offer:

▪ Mental health conditions (e.g. use of DMHEF)

▪ Sensory impairments

▪ Drug or alcohol dependency or both

▪ Physical disabilities

▪ Learning disabilities

▪ Low literacy levels

▪ Low language skills

▪ General difficulty in communicating

▪ Homelessness

The customer’s personal circumstances can also make them vulnerable. For example, people who have:

▪ been impacted by COVID-19

▪ just left prison

▪ just left hospital

▪ chronic gambling problems

▪ a history of being in care

▪ been recently bereaved

▪ recently suffered domestic violence or threats

▪ recently been a victim of crime/fraud (e.g. identity theft)

It is recognised that a vulnerable customer may meet multiple characteristics of vulnerability and require several of the VRS sub-flags to be triggered.

The IP and trained staff members may sometimes be required to ask a customer very personal questions and it is important to do so in a sensitive way. Where special category personal data (As defined by the DPA 2018) is captured then the reason for the use of the information should be recorded.

Key considerations:

▪When giving information it is essential that it is presented in a clear and concise way, using language that they can understand, and pitching what you say at a level, that suits them, without being patronising.

▪ It is necessary to be aware of the consumer’s/customer’s reactions to ensure that they understand what is being said.

▪ We want the customer to feel quite clear and confident about what they have been told and what to do next.

▪ We take into account the individual needs of the customer; they know best what their needs are, so ask them rather than assume.

▪ When it might be appropriate to recommend the use of an appropriate interpreter services, acting on behalf of the customer

▪ For a customer who has physical disabilities or sensory impairments, always take into account their health, disability or other needs

The IP and staff should always take quality notes and (if advice is delivered over the phone or through Teams/Zoom) record calls to review afterwards the most effective strategy for communicating with the client in future that both meets their personal needs and the communication mechanisms available. The notes should include capturing the how far into the call (e.g. 12th minute of the call) an event occurred to make quality assurance of the case more straightforward.

It is important to determine whether the vulnerability identified whilst in dialogue with the consumer/customer affects their ability to manage their money. If the person is receiving treatment or support for this then does the treatment or support affect their ability to manage their money (e.g. what is the most appropriate payment method if you are distributing client money)?

A customer that is determined as vulnerable or particularly vulnerable should be clearly marked on the internal customer management system. The nature of the vulnerability should also be detailed, but mindful of the fact that this could be treated as special category personal data in the context of the DPA 2018.

This policy recognises the importance of the IP and staff having up-to-date, relevant and accurate information about customers that may be regarded as vulnerable or particularly vulnerable. We remain aware of the sensitivity of the data we are collecting and we will ensure that it is kept securely and only used for the stated purposes in accordance with our own Data Protection Policy and Privacy Policy, which is available on our website.

In line with the IPA ‘Dealing with Vulnerable Individuals Aide Memoire for IPs’, we have adopted the key practice clearly documenting the reasons for any decisions in conducting an individual insolvency and explain the factors we have taken into account. We understand from a regulatory perspective that this will go a long way to demonstrate that we have acted with due care and competence.

Staff and associates may need to take action to respond to consumer/customer disclosures of suicide. This is subject to a separate policy and procedure.

7. Further information

MAT debt adviser guidance – June 2016

Mental capacity guidance – FCA Handbook:

CONC 2.10 Mental capacity guidance - FCA Handbook

MALG – Mental health and debt guidelines

https://malg.org.uk/resources/malg-mental-health-and-debt-guidelines/

FCA final vulnerability guidance

Money Advice Trust – Vulnerability hub

https://www.moneyadvicetrust.org/training-and-consultancy/vulnerability-resources/

IPA – IPA Vulnerable IP Policy (July 2020)

The IPA, as a Recognised Professional Body (RPB), Anti-Money Laundering Public Body Supervisor, and a member services organisation, wishes to support its members and licensed IP population through any personal difficulties, helping them navigate through challenges that may arise, so that their work and cases are conducted properly, and so that they can continue to meet their statutory obligations.

https://insolvency-practitioners.org.uk/wp-content/uploads/2020/07/VIPP-Post-Board-07-2020.pdf

IPA - Dealing with Vulnerable Individuals Aide Memoire for IPs

https://insolvency-practitioners.org.uk/uploads/documents/94cf32daed5d138f4a8c7211e66b1973.pdf

Advice Line:

(NI & ROI) 02891 814890

(UK Mainland) 02920 346530

Why Choose us?

- Accredited Advisors

- Free advice

- Nationwide Coverage

- Professionals that are here to help

- With you every step of the way

Would you like some help?

Our team are waiting for you to call and help you recover your financial position

Contact Us